Analysis Ovintiv Builds Major Alberta Montney Liquids Foothold

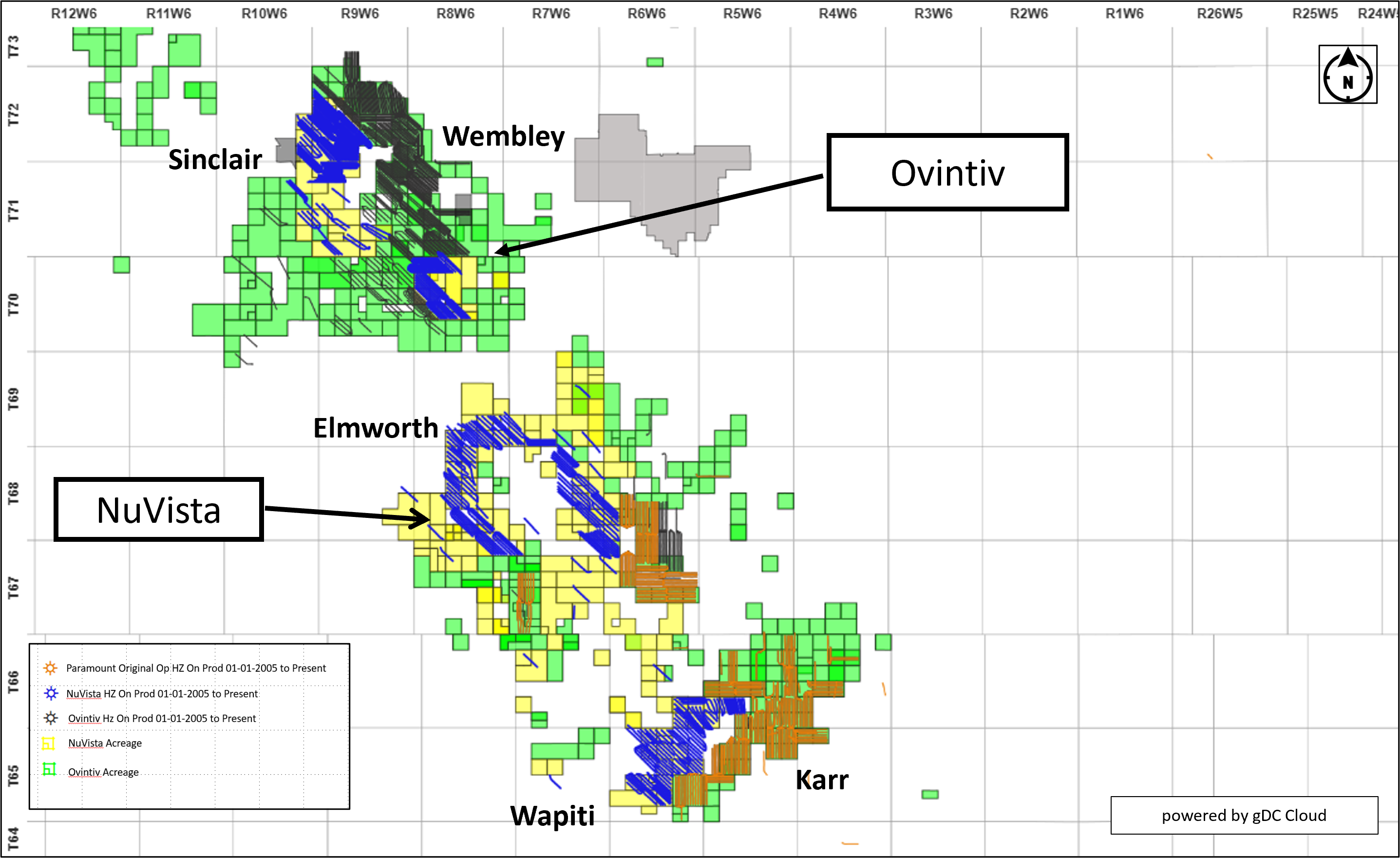

Ovintiv Inc. completed this week its US$2.7-billion acquisition of NuVista Energy Ltd., with the deal adding 140,000 net core acres and over 900 potential drilling locations in the liquids-rich window of the Alberta Montney.

Current production from the assets is approximately 100,000 boe/d, including 25,000 bbls/d of condensate.

The NuVista acquisition followed Ovintiv’s $3.3-billion acquisition of Paramount Resources Ltd.’s Grande Prairie Montney assets that closed in January 2025. That deal added approximately 110,000 net core acres, along with approximately 900 drilling locations and 70,000 boe/d of production.

The two deals combined have almost doubled Ovintiv’s core Montney acreage from 260,000 acres prior to the Paramount deal to 510,000 acres, giving it 15 to 20 years of liquids-rich drilling inventory.

All of its liquids-rich acreage is in the Grande Prairie region, with accounts for over 90 per cent of Alberta condensate production.

It also has about 30 years of leaner gas inventory in the B.C. Montney at current production rates.

The acquisitions have increased Montney production from approximately 240,000 boe/d to current levels of 400,000 boe/d, including 85,000 bbls/d of oil and condensate and 1.75 bcf/d of natural gas.

While Ovintiv has yet to release its 2026 guidance, the company is expecting to run a maintenance budget in the Montney, said president and chief executive officer Brendan McCracken in announcing the deal in late 2025.

It anticipates running an average of six rigs and one to two frac crews in the Montney in 2026. Wells are expected to be split equally between its original Pipestone, legacy Paramount and NuVista assets.

Source: gDC Wells Spud Dashboard

The company has capacity to increase oil and condensate production to 100,000 boe/d if markets shift, McCracken said in late 2025.

“I think today it’s fair and reasonable to say there is not a market demanding more barrels or BTUs be produced, and so that signal calls for a maintenance level investment.”

The company also looks at whether it can get better cash flow per share by adding activity versus buying back shares, he added.

“And again, that signal is telling us it’s a better option for our shareholders to buy the shares back to generate that cash flow per share growth.”

“When we incorporate these NuVista assets, we’re going to fold them into that same capital allocation strategy. We’ll be slowing that rate of growth investment down and running the assets for free cash generation if the environment continues to be the same.”

Instead of growth, Ovintiv will be focused on driving down development and operating costs, while maximizing realized prices from the assets, said chief operating officer Greg Givens.

“We expect to capture about $100 million in durable annualized free cash flow synergies. About half of the synergies are from lower capital costs. We expect to achieve a savings of $1 million per well consistent with our current Montney well costs from streamlined facility design and faster cycle times.”

Givens added: “The balance of the synergies come from other non-well capital savings, lower production costs driven by enhanced scale and connecting the wells to our Grande Prairie operations control center — where we use automation and in-house AI tools to optimize production and reduce downtime — as well as lower overhead.”

Ovintiv has a playbook in place to integrate the assets, which it used successfully on its Paramount acquisition, he said.

Since closing on the Paramount assets last January, the company has achieved its target of cutting costs by $1.5 million per well.

Approximately $1 million of savings came from drilling, including $600,000 resulting from its high efficiency casing design and $400 million from faster drilling times, partially due to a change in drill bits.

“We’ve taken out 10 days compared to the previous operator, and we’re now 15 days from spud to rig release,” Givens said.

Ovintiv has reduced completions costs by $300,000 per well, mostly resulting from pumping 30 per cent less fluid than the previous design and self-sourcing sand, he added.

Source: gDC Frac Analysis

The remaining $200,000 has come from improved facility design needing 85 per cent less structural steel and with building times twice as fast the previous design.

It expects similar results with the NuVista assets, he said.

“Immediately after close, we’ll be connecting their rigs up to our drive centre where we’ll use in-house algorithms and AI to further refine our drilling efficiencies as well as our cost based on things we’ve learned here and in the U.S. We think that’s going to drive several days out of drill times.

“On the completion side, we’re going to utilize our real-time frac optimization centre, which will refine pumping schedules, shorten cycle times. Our use of local sand there in the basin … should also generate some really good cost savings shortly after close.”

Ovintiv has identified 620 premium locations that assume spacing of 10 to 14 wells per section, with 310 upside locations that assume up to 16 wells per section in the most prolific areas, plus additional infill opportunities, on the NuVista assets, Givens said.

“This is consistent with the development approach taken on our legacy assets, including the Paramount assets.”

The company also sees opportunity to drill and complete longer laterals as a result of the deal, he said. Ovintiv has been extending laterals in the Montney the last five years.

“If you look at the map, this is just ripe for opportunities to lengthen laterals across lease lines, and to share infrastructure.”

He added: “We’ve got some shared acreage that actually had a shared working interest between Paramount and NuVista historically. We’ll be able to make those 100 per cent working interest wells, extend lateral lengths, develop that very efficiently.”

AI, automation to drive down operating costs

The company also expects to drive down operating costs on the NuVista assets, Givens said.

“We’ll do just what we did on the last transaction. We’re going to connect the wells to our operations control centre in Grande Prairie very quickly and inexpensively. And from there, we’ll be able to optimize production using our in-house AI tools and algorithms on all the wells with set points on artificial lift, those types of things.

“But also, what we found to be very effective is the automation that we put in place. We can not only shut in wells remotely, but also bring them back online in minutes.

“When inevitably you do have a downtime or a turnaround, we can bring our wells back online faster than anybody else in the industry up there. And what that does is just really increases our uptime. So, you’ll see a production benefit there as well as a cost reduction.”

Source: Evaluate Energy

Deal should drive better average gas prices

Condensate is the key economic driver of the deal. While condensate production accounted for 25 per cent of NuVista’s production, it drove two-thirds of revenues in the first half of 2025.

But the deal should also improve Ovintiv’s average realized gas prices out of the Montney, said Givens.

Pro forma, Ovintiv’s 2026 AECO exposure will drop from around 30 per cent of its Montney gas to around 25 per cent.

“They have done a great job of building out a diversified portfolio of firm transportation contracts to markets across North America for about 250 mmcf/d of their natural gas volumes. They’ve received strong realized pricing as a result. Year-to-date, as of the end of the second quarter, the pre-hedge gas price realization was approximately 180 per cent of AECO.”

NuVista also has an ongoing hedging program in place, he added.

“In addition, they have JKM link contracts for 21 mmcf/d starting in 2027.”

Source: Evaluate Energy